The US Fed confirmed today that it is likely to begin to pare back the close to $4.5 trillion of assets on its balance sheet (mostly government debt and mortgage backed securities). In order to avoid too much market impact it is likely to allow certain issues to run off, without reinvesting the proceeds as they currently do, as opposed to actively selling the securities in the open market. This “gently, gently” approach suggests an institution wary of instigating a further “taper tantrum” such as was witnessed in late 2013.

It also signaled that it was likely to raise rates for the fourth time since the recession at its June meeting if the economy stays on track – a move that has been widely anticipated in markets and most likely already discounted in to valuations.

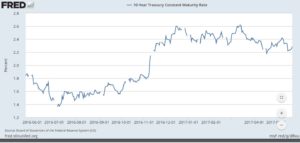

However as the chart below indicates despite the current trajectory of rate rises, there has been little movement around the 10 year end of the curve since the beginning of the year – with 10 year rates hovering between 2.2 and 2.4%. This suggests that the long-term path for interest rates is by no means clear and that perhaps the rumors of the demise of the “30 year bond bull market” have been exaggerated.

So what has the core fixed income investor’s experience been year to date? With the Barclays U.S. Agg index up around 1.59% as of the end of April active strategies have added up to 100 bps year to date, mostly by increasing credit exposure in areas such as high yield, bank loans and EMD and substituting mortgage backed securities for US government bonds. From a technical standpoint managers are experiencing few outflows – mainstream fixed income investors seem somewhat ambivalent about the low return stream, citing the ubiquitous low rates of return. Equally, retail investors, who may have chased yields in this area when total returns hovered around 6 – 7% seem content to stay there, for now, with little to no outflows from retail investors or other “tourists” being experienced.

It may be a case of the “best of a bad lot” or even reflective of increased jitters in markets and a need to hold some ballast or safety in the event of a risk-off investor flight. For our part we are sticking with our core fixed income allocation, but seeking to understand, very well, how those assets are managed and where excess return is derived. We are also scrutinizing each of our unconstrained managers in the same way to determine who is bullish on EMD, who is reining in risk and who is playing with duration. It is clear that fixed income still works well as one end of a bar bell and that the demand picture looks to remain robust.